Skip to main content

Skip to main content

Hurricane season is in full swing in Houston and the National Oceanic and Atmospheric Administration (NOAA) just put residents on high alert. Thanks to record-warm surface water temperatures, NOAA doubled their estimate for hurricane activity in the Gulf of Mexico – from 30% to 60%. Read on for best practices for community associations hurricane preparedness from RISE Association Management.

Hurricane damage – who pays when storms hit HOA communities and condos?

Most hurricane damage to condominiums and in HOA communities is paid for out of pocket. That is because while many areas may be “affected” by the named storm, they are may not be located in the direct path and thus the type of damage they sustain is less likely to be of the catastrophic variety necessary to reach the high named storm deductibles set by their policy. Even forgettable storms can cause very costly repairs to condominiums and HOA community property. Insurance deductibles for windstorms, particularly named storms, have steadily risen along the Gulf Coast; it now takes a significant event to reach many policy deductibles, leaving your HOA and condo board to pay for uninsured costs out of pocket.

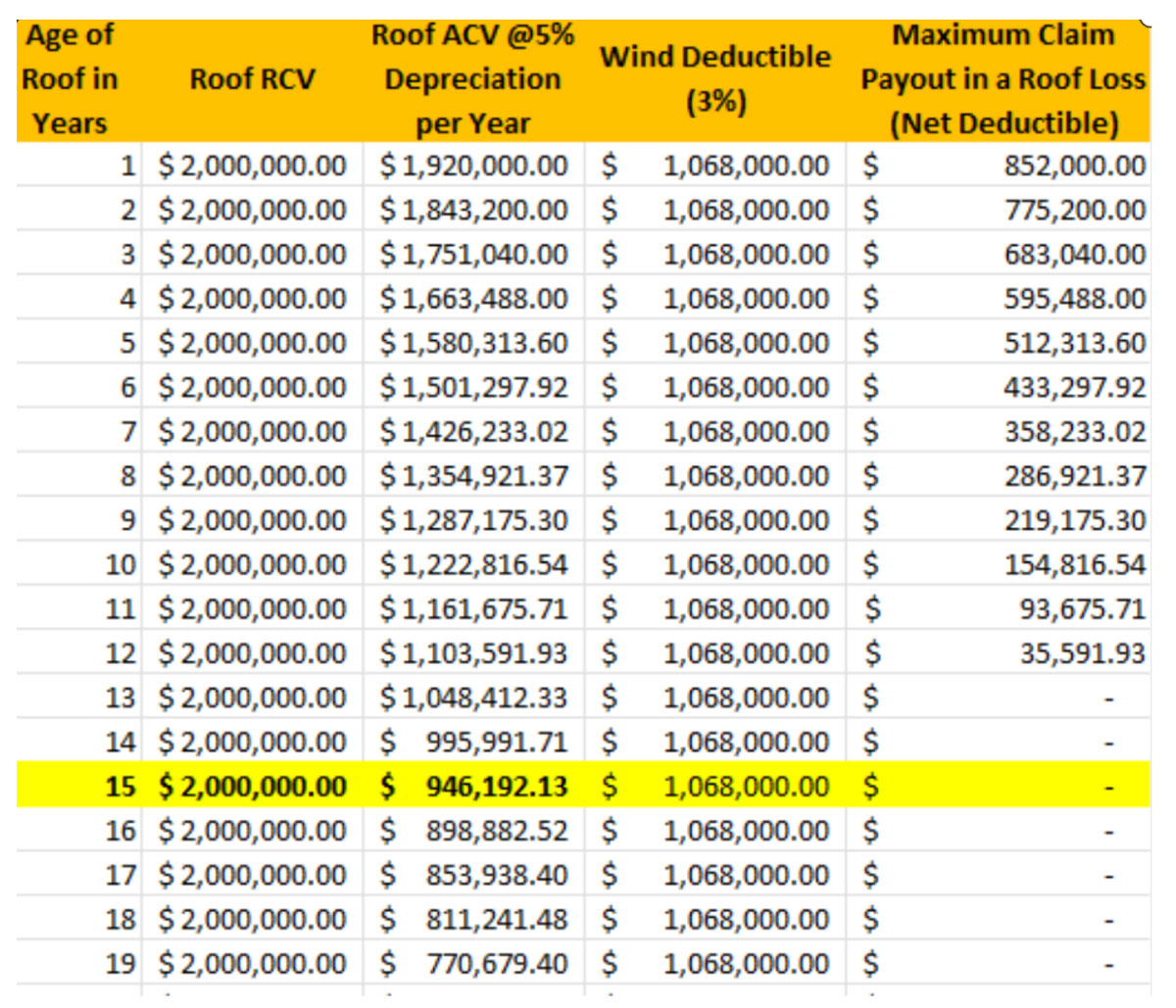

In addition, many homeowners’ association insurance policies cover roofs on an “actual cash value” if they’re older than 12 years versus those which offer “replacement cost value.” Put simply, your roof loses value at 5% each year. So, by the time it reaches 15 years old, even a total loss, meaning it requires complete replacement, would only be insured for 47% of its original value. This is the Actual Cost Value (ACV), whereas the Replacement Cost Value (RCV) is still $2,000,000. In the scenario below, that is still below the named storm deductible, meaning the entire loss of $2,000,000 would be paid out of pocket.

This is one of the most common exposures homeowners’ associations and condo associations face, but most are unaware of it until a claim is made. These situations often require a special assessment or dipping into your association reserves. The most common type of damage occurs to amenity centers or condominium roofs, which if older than 10 or 15 years, may only be paid on an actual cash value basis rather than a replacement cost basis. Outdoor property such as pool or patio furniture, even if valued on a replacement cost basis, is often unlikely to meet minimum windstorm deductibles.

An ounce of preparation is worth a pound of cure for condos and HOAs

What’s in a name? When it comes to hurricanes, it’s wind. The expected sustained wind speed is what determines different storm classifications. Tropical cyclone is the umbrella term for an organized system of clouds and storms over tropical waters. National Hurricane Center classifies cyclones as follows:

- Tropical depression – tropical cyclone with maximum sustained winds 38 mph or less

- Tropical storm – tropical cyclone with maximum sustained winds of 39 – 73 mph

- Hurricane – tropical cyclone with maximum sustained winds of 74+ mph

- Major Hurricane – tropical cyclone with maximum sustained winds of 111+ mph

Wind can impact operations in high-rise condominiums and in communal areas of HOA-managed neighborhoods. This is why it is critical that homeowners association management companies like RISE take the following precautions when expected wind speeds are 40+ mph. Ask your property manager about specific protocols in your community.

- Insurance Review- Review homeowners and condominium association master insurance policy prior to hurricane season. Ensure that homeowners and condominium unit owners understand the level of risk they carry for special assessments. These policies NEVER cover your personal belongings.

- Elevators- may be shut down to prevent passengers from being trapped during a loss of power or to prevent damage to the cabs from water intrusion. [watch video tutorial]

- Mechanical Systems- including air conditioning systems and domestic water pumps, may be shut down to avoid damage to the pumps which occurs when water may be interrupted.

- Gas and Boilers- may be shut down prior to a storm to prevent possible gas leaks as a result of wind damage. This means you may not have access to hot water until the systems are restored.

- Automatic Gates- may be held in the open position to avoid ingress/egress disruptions in the event of a loss of power. [watch video tutorial]

- Pools and Spas- depending on the type of storm, pools and spas may be closed, drained, and the pumps shut down to prevent damage from debris entering the system. [watch video tutorial]

- Other Amenities- may be shut down or closed to secure property and protect equipment.

Hurricane preparedness for community associations before the storm

Planning ahead can save precious time when a major storm is on the way. Actions taken in advance can protect individual residents and the entire community. Remember, together we RISE!

- Keep your contact information current with your community manager. Contact RISE with your preferred telephone, email, and mailing address at riseamg.com.

- If interested, sign up to be an Emergency Volunteer. Volunteers help with reporting property damage, assisting other residents, securing building/facility systems, and providing lodging for non-residential storm responders. Go to riseamg.com to volunteer.

- Get on the mobility-impairment list. This list goes to the Fire Department when responding to a building emergency; it covers any resident within your unit. Request mobility assistance by reaching out to your HOA manager.

- Prepare an emergency supplies bag. Click here for a list from Texas Ready on what to include. Items like water and toilet paper will be in scarce supply immediately before a storm makes landfall.

- Clear your balcony and outdoor areas. This is to prevent items from becoming projectiles in high winds. This includes heavy items like satellite dishes, potted plants, and furniture.

- Remove vehicles from any flood prone areas. Identify somewhere on higher ground in advance where you can park vehicles, and designate a driver to assist with the drop-off.

- Review your insurance coverage. Association insurance policies vary in coverage.

Best practices for community associations following a major storm

When wind or high water strikes, it’s important to assess the damage quickly AND SAFELY.

- Photograph any damage to your property and association-maintained property.

- Mitigate damage to the best of your ability and immediately report it. Contact your Association Manager directly.

- Allow prompt access to your unit for damage inspection. Please be certain you or a designated individual are available to provide access immediately after a storm. Entry to inspect and mitigate damage is time sensitive and delays may result in further damage.

** All owners have a responsibility to attempt to preserve property affected by a loss to the extent possible. However, never compromise your safety to salvage property.**

We’re no match for Mother Nature. Personal safety is our #1 concern. With preparation and processes already in place, you can lessen the severity of loss and get on a rapid road to recovery. RISE takes the burden off HOA and condo boards to make sure communities thrive before, during, and after the storm.

Still have questions? Contact RISE Association Management Group at 713-936-9200 or