Smarter Coverage, Lower Costs, and a Proven Strategy

Introduction to the RiseShield Master Insurance Program

Insurance costs for HOAs and condominium associations have skyrocketed in recent years. Between tighter underwriting standards, rising claims, and shrinking carrier appetites, many associations have struggled to find affordable, comprehensive coverage often resorting to special assessments to fund insurance or simply reducing coverage.

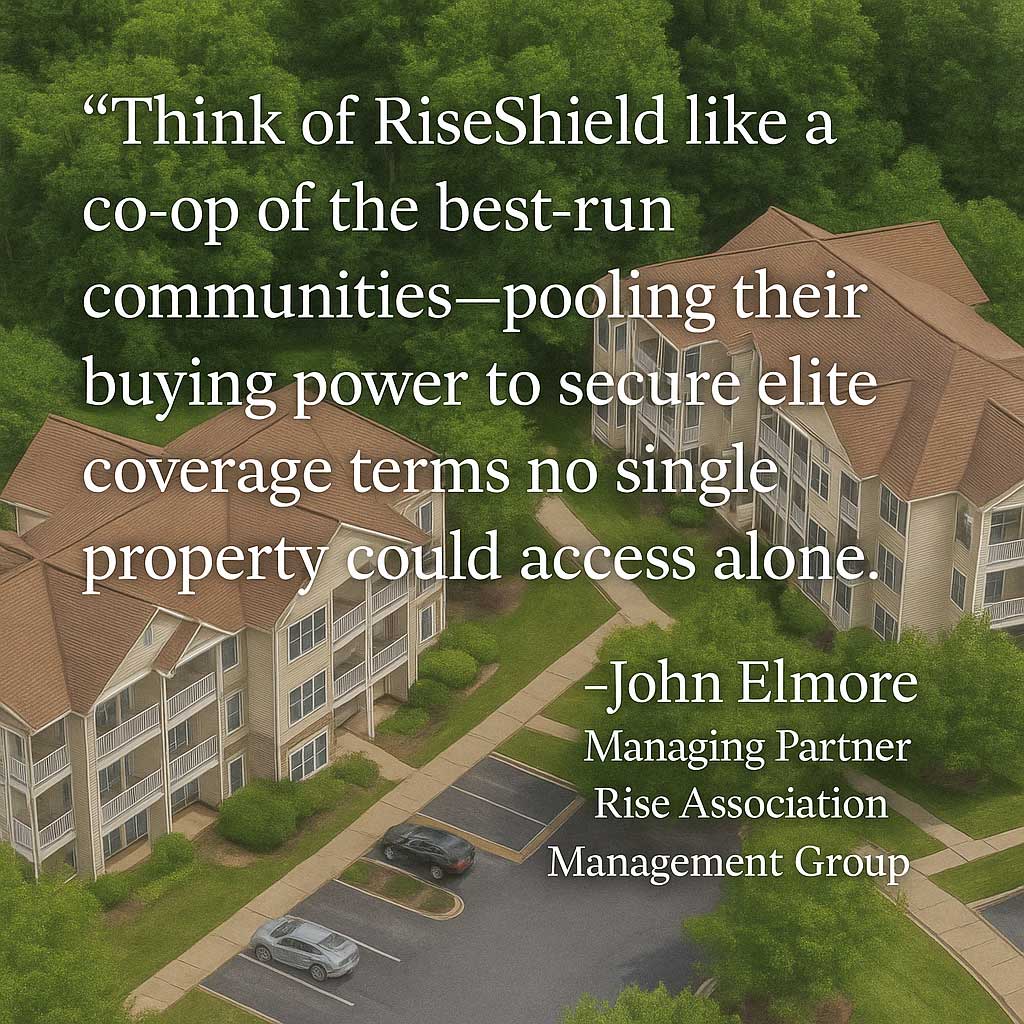

To help our communities solve this problem RISE has leveraged its size, scale, and risk management expertise to create the RiseShield Master Insurance Program for a select group of preferred clients invited to participate—those with strong operational governance, proactive maintenance, and low loss history. This creates a curated portfolio of well-managed associations that collectively enjoy preferred pricing and enhanced protection while maintaining lender compliance and individual limits for each insured community. Combined with risk mitigation and education by the RISE Team, which includes HO-6 policy requirements and homeowner education, we ensure that communities actively participate in reducing claims, keeping costs down for everyone.

Recent changes as of April 2025 to the Fannie Mae Selling Guide have made the RiseShield Master Insurance Program eligible for FNMA financing—officially recognizing properly structured master insurance programs such as the RiseShield Master Insurance Program can both provide adequate protection to homeowners, community associations, and FNMA if they meet defined requirements and deliver great value. Read more about Fanne Mae’s latest updates here: April 2025 Fannie Mae Selling Guide.

This deep dive explores how RISE’s program works, the myths and realities of the RiseShield Master Insurance Program, and the measurable benefits our clients’ experience.

Challenges for HOAs/COAs in Today’s Insurance Market

Homeowners associations and condominium boards are facing a perfect storm:

- Premiums have risen at an alarming rate nationwide for years as insurance carriers react to rising property losses, persistent inflation, and widespread undervaluation of properties.

- Fewer carriers are willing to underwrite condo and HOA policies, reducing competition according to Yahoo Finance’s Claire Boston. Read more here: Yahoo Finance: Insurers are Dropping HOAs and Threatening the Market.

- Higher deductibles, often employed to offset costs of rising premiums, shift more financial burden onto communities and their members creating larger coverage gaps and risks.

- Stricter underwriting guidelines mean some properties are being denied coverage altogether or coverage has become completely unaffordable.

Adding to this complexity is updated guidance from Fannie Mae that now makes it explicitly unacceptable to limit coverage for any required peril—including fire, windstorm, hail, explosion, and vandalism. FNMA now requires full Replacement Cost Value (RCV) for all these perils and prohibits exclusions, restrictive sublimits, or partial coverage for them. This means that many previously compliance insurance structures—such as policies that cap windstorm losses or exclude certain risks—are no longer eligible.

As a result, associations must be more strategic and forward-looking in how they structure insurance. HOAs need to take control of their risk management strategy—and that’s where the RiseShield Master Insurance Program comes in.

RiseShield Master Insurance Program Solution

Through our partnership with Archer Risk Services, RISE structures a RiseShield Master Insurance Program that delivers significant advantages for associations:

✅ Lower Insurance Premiums – By leveraging our size, active risk mitigation, using a select group of preferred risk clients, we negotiate bulk discounts and better coverage terms which we can pass on to our client base as a value add of being a RISE client.

✅ Broader Coverage & Fewer Exclusions – A well-structured master policy often provides more comprehensive coverage than fragmented standalone policies.

✅ Streamlined Claims Handling – Our program centralizes claims management, ensuring faster response times and better outcomes.

✅ Risk Management & Compliance Support – We help HOAs stay ahead of underwriting changes and compliance requirements.

Separating Fact from Fiction

Fiction: The RiseShield Master Insurance Program is non-compliant with lender requirements.

With updated guidance from Fannie Mae in April 2025, Policies Covering Multiple Unaffiliated Projects are now eligible for FNMA financing—provided each individual project has a clearly defined, dedicated coverage amount within the master policy. This long-awaited change opens the door for correctly structured insurance programs to offer affordable coverage while retaining FNMA and other lender underwriting approval.

As long as each project retains its own governance and financial independence, they may now participate in shared policy arrangements so long as their insurable value is allocated distinctly.

This is a major step forward and one that validates the model RISE has been championing for years.

Fiction: The RiseShield Master Insurance Program means HOAs lose control over their coverage.

RISE’s program ensures that each HOA is named as an insured on the policy and maintains control over coverage levels, claims decisions, and risk management strategy while benefiting from economies of scale.

Fact: The RiseShield Master Insurance Program reduces costs and stabilizes premiums.

By leveraging a master policy schedule, HOAs in the program gain access to bulk pricing and risk distribution advantages that single policies cannot provide.

Fact: The RiseShield Master Insurance Program works best with proactive risk management.

The best results come when associations actively manage claims exposure—which is why RISE incorporates homeowner education and HO-6 policy requirements into our strategy.

A unique feature of RISE’s RiseShield Master Insurance Program is that eligibility requires participating condominiums to implement loss prevention and mitigation strategies proactively. RISE’s role is to help HOA’s carry these out on the HOA’s behalf within set budgets. This provision is essential to the program’s success: insurance carriers are underwriting RISE as a management company, not just the individual properties. As such, RISE must have the authority to take immediate and effective steps to reduce or limit damage when risk events occur.

This trust and control is a key reason the program achieves significant cost savings—because insurers know RISE is empowered to act decisively on behalf of the properties we manage.

Understanding Fannie Mae’s Rules

Fannie Mae has revised its rules many times in recent years as it pertains condominium association lender compliance. Read more recent changes here: Is Your Condo Association with Fannie Mae Compliant Rise AMG. With the April 2025 update, Fannie Mae has formally acknowledged that shared master insurance policies covering unaffiliated condominium projects may now qualify for financing, provided that the policy structure clearly allocates dedicated coverage amounts to each participating project. This significant revision represents progress for associations seeking cost-effective solutions without compromising compliance.

Fannie Mae has also refined its coverage requirements to ensure adequacy and eliminate ambiguity. Condominium master insurance policies must now:

- Be written on a Replacement Cost basis, insuring 100% of the insurable replacement cost of the project.

- Include Special Form coverage (previously referred to as “All Risk”) for perils such as fire, windstorm, hail, explosion, riot, aircraft, vehicles, smoke, and vandalism.

- Include Ordinance or Law coverage to meet current building code compliance standards.

- Maintain deductibles of no more than 5% of the policy’s coverage amount.

- Include Fidelity insurance for HOAs with 20+ units, covering at least three months of assessments and all reserve funds.

- Crime Coverage must cover the property manager as an insured if they handle HOA funds.

- Include Boiler & Machinery/Equipment Breakdown coverage for central systems (e.g., elevators, HVAC), with at least $2 million in coverage if available in the market.

- Carry Directors & Officers (D&O) liability coverage to protect board members.

- Provide Umbrella coverage of at least $1 million if the project includes high-risk amenities such as pools or playgrounds.

- Carry Flood insurance at 100% replacement cost with a maximum $25,000 deductible if located in a FEMA-designated Special Flood Hazard Area.

Importantly, Fannie Mae has clarified that if certain endorsements or coverages—such as Inflation Guard or Boiler & Machinery—are not available in the current marketplace, they are not required for compliance. Associations must simply document the market unavailability as part of their lender disclosures. This provides greater flexibility in volatile insurance markets while still maintaining the core principles of sound coverage.

Additionally, policies may not limit coverage for any of the required perils, either by exclusion or restrictive sublimits. For example, windstorm losses must be fully insured without arbitrary caps. Coverage forms that exclude wind or apply non-standard limitations are no longer considered acceptable, even if the peril is technically included. This ensures that associations remain adequately protected against regional risk exposures.

Why RISE’s Master Program Meets FNMA’s 2025 Selling Guide Requirements

RISE’s RiseShield Master Insurance Program was intentionally structured to align with Fannie Mae’s stringent requirements for condominium project eligibility. Here’s how our program ensures compliance:

- The coverage amount dedicated to each community association is 100% RCV per occurrence which provides sufficient coverage to cover the full replacement cost value of property including the common elements and residential structures, as required under FNMA guidelines.

- The coverage amount dedicated to each project is sufficient to cover the full replacement cost value of the project improvements including the common elements and residential structures, as required under FNMA guidelines.

- Uses the Special Causes of Loss form to include all FNMA-required perils, as required under FNMA guidelines.

- Incorporates Ordinance or Law coverage and Boiler & Machinery coverage, as required under FNMA guidelines.

- Features deductibles well below FNMA’s 5% maximum, enhancing both affordability and compliance, as required under FNMA guidelines.

- Ensures each property’s insured value is derived from a formal valuation tool, confirming 100% RCV is achieved and documented.

- Includes insurance trustee language in the policy, a requirement for FNMA-eligible projects.

- Provides a waiver of subrogation clause that protects unit owners from insurer recovery actions, aas required under FNMA guidelines.

- Establishes that the master policy is the primary policy, even in situations where a unit owner has a personal policy covering the same risk or property, as required under FNMA guidelines.

- Includes a Severability of Interest clause, which ensures no claim or misrepresentation made by one unaffiliated project can invalidate or reduce the coverage available. Each insured association is treated as if they are separately insured, as required under FNMA guidelines for

- Ensures that coverage for each project remains individually enforceable regardless of the actions or circumstances of the others.

This structure aligns directly with Fannie Mae’s updated compliance criteria for multi-project insurance arrangements and is a core feature of how RISE’s RiseShield Master Insurance Program protects every insured community.

The Role of HO-6 Policies in Protecting Associations

One of the biggest risk factors for HOAs is underinsured homeowners—which is why we require and enforce HO-6 (unit owner) insurance policies as part of our approach.

🔹 Why HO-6 Policies Matter:

- They provide interior coverage for unit owners, reducing the association’s liability.

- They cover unit owner negligence claims, protecting the HOA from unnecessary losses.

- They ensure owners contribute to deductibles, preventing large financial hits to the HOA.

🔹 How RISE Educates Homeowners:

- We provide clear policy guidelines on required HO-6 coverage limits.

- We conduct educational sessions to help homeowners understand their responsibilities.

- We work with lenders and insurance agents to ensure compliance at the time of purchase and renewal.

The result? Fewer claims, lower premiums, and stronger financial stability for the community.

The Bottom Line: Why HOAs Choose RISE’s RiseShield Master Insurance Program

At RISE, we don’t just manage associations—we protect them. Our RiseShield Master Insurance Program, combined with HO-6 policy enforcement and proactive homeowner education, creates a sustainable insurance solution that delivers real financial benefits.

If your HOA is struggling with rising premiums, noncompliance with lender requirements for insurance coverage, unpredictable claims, or inadequate coverage, it’s time to explore a smarter way forward. Contact us today to see if your community qualifies for RISE’s RiseShield Master Insurance Program. Get in touch with RISE or connect with our partners at Archer Risk Services.